The Climate-Integrated Enterprise

Inside Integrated Value Planning

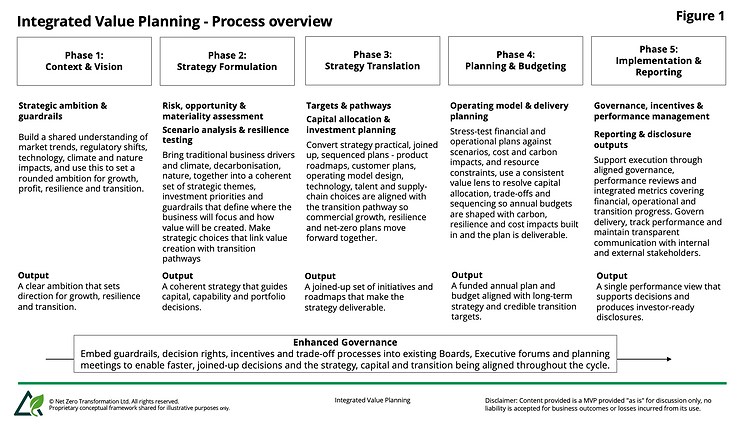

Integrated Value Planning helps strategy, finance and sustainability work as one planning system.

Energy volatility. Water stress. Carbon pricing. Insurance repricing. Supply chain concentration. Shifting customer requirements. Tougher disclosure expectations.

These are no longer sustainability side issues. They affect margins, contract competitiveness, asset values and access to capital. They influence how durable a business model looks over the next decade.

Yet most corporate planning systems were built for a different operating environment. They assume relative stability in input costs, regulation and physical conditions. Climate has introduced structural uncertainty, but in many organisations it still sits alongside the core planning cycle rather than inside it.

When I stepped back from leading large transformation programmes to focus more explicitly on climate and business integration, I expected to find a motivation gap at board level. In practice, that has rarely been the case. Most executive teams understand the scale of the transition challenge. They have set targets. They publish transition plans. They respond to investor questionnaires.

The gap appears later.

It shows up when strategy becomes budgets, when initiatives compete for funding and when trade-offs are made under time pressure. The question is not whether climate matters. It is how to manage climate risk and regulatory pressure alongside every other commercial priority without creating parallel processes or overwhelming leadership teams.

The Integrated Value Planning Framework was developed in response to that practical problem.

What Integrated Value Planning does

The Integrated Value Planning Framework does not create a new sustainability process. It adapts the planning and governance processes organisations already rely on so that strategy, finance and sustainability operate as one decision system. See Figure 1.

Climate, carbon, water and resource constraints are treated as business variables. They sit alongside demand forecasts, cost assumptions and competitive positioning. The purpose is not to elevate climate above other priorities. It is to ensure it is not invisible when capital is committed.

The objective is straightforward: improve trade-offs, direct investment more intelligently, reduce hidden exposure and identify new sources of value.

Anchoring strategy in operating reality

All strategic planning begins with context. In an integrated approach, transition pressures are considered from the outset rather than appended at the end.

Tools such as scenario analysis and materiality assessment are used to answer commercial questions. Where are we exposed to carbon pricing? Which parts of the portfolio are vulnerable to energy volatility? How might water stress or physical disruption affect operating capacity? Where could regulatory change alter competitive dynamics?

These are not disclosure questions. They are portfolio questions.

By exploring them early, ambition is anchored in operating reality. Growth targets reflect structural constraints and opportunities rather than assuming that the future will resemble the past.

Guardrails that shape decisions

From there, the executive team agrees a small number of guardrails. These are explicit decision criteria that define acceptable exposure.

For example, what level of carbon intensity is acceptable within the product portfolio over time? How concentrated can supplier exposure be in high-risk geographies? What reliance on volatile energy inputs is tolerable? How should capital be sequenced to manage transition risk.

Without clear guardrails, exposure is acknowledged but rarely acted upon. With them, risk parameters influence product design, sourcing strategy and capital allocation before proposals are fully developed.

As commercial plans and operating models are built, these criteria are already embedded. Transition initiatives are sequenced alongside other transformation priorities rather than managed as a separate sustainability track competing for attention and funding.

Bringing finance fully into the picture

Financial integration is critical. Investment cases should be stress-tested against carbon and energy scenarios rather than relying solely on single-point forecasts. Where appropriate, internal carbon pricing can be used within capital appraisal to reflect expected transition costs.

When a proposal meets financial hurdle rates but breaches agreed guardrails, that tension is addressed explicitly. The trade-off is made consciously rather than discovered later through reporting or investor challenge.

This does not require new committees. It requires existing investment and governance forums to consider a broader set of variables consistently. The discipline lies in making trade-offs visible.

The result is not perfection. It is improved decision quality.

Using regulatory frameworks to strengthen decisions

Regulatory and voluntary frameworks such as the Transition Plan Taskforce guidance, UK SRS, CSRD, ISSB, TCFD, TNFD and SBTi require detailed analysis. In many organisations that analysis sits in parallel sustainability workstreams and culminates in reporting outputs. See Figure 2.

In an integrated planning model, the same analytical work informs strategy and capital allocation.

Scenario modelling shapes financial assumptions early in the planning cycle. Materiality assessments influence portfolio focus. Transition commitments are costed before budgets are approved rather than retrofitted afterwards.

Scope 3 emissions illustrate the shift. In many companies they remain a reporting metric. In an integrated model they become an operational signal. A concentrated, carbon-intensive supplier base may indicate exposure to energy volatility, future carbon border adjustments or regulatory tightening. When that signal is embedded in sourcing strategy and financial sensitivities, it influences contract structures, diversification and product design long before it appears in a sustainability report.

The same logic applies to regulatory compliance more broadly. Managed in isolation, frameworks add complexity and reporting burden. Integrated into planning, they strengthen capital allocation and long-term competitiveness.

A practical reference model

Integrated Value Planning is a reference model that can be used to stress-test existing planning processes, governance structures and data flows. It is not intended to replace established systems but to evolve them.

The focus is incremental improvement. Strengthen the link between strategy, financial modelling and transition risk. Make trade-offs visible. Align growth, resilience and decarbonisation within one decision system so they reinforce rather than compete.

Businesses will play a decisive role in addressing the climate challenge. Progress will depend not only on targets and disclosures but on whether climate variables genuinely shape strategy and investment decisions.

If they do, resilience improves and risk is priced more accurately. If they do not, exposure remains hidden until it surfaces through margin pressure, asset impairment or investor challenge.

The question for leadership teams is not whether they have a transition plan. It is whether transition economics are embedded in the decisions that determine the future shape of the enterprise.

That is the work of integration.